Decimalisation

| DECIMALISATION: 100% complete | |||

|

|||

| Decimal | Non-decimal | ||

| All coins are decimal. | |||

| All postage stamps are decimal. | |||

| All financial transactions are decimal. | |||

Decimalisation and metrication

Currencies, or the systems of money, in common use in the world, are not included in the metric system. However, decimalisation, or the conversion from a non-decimal currency to a currency based on multiples of 10 and 100, bears similarities to metrication. Both involve the switch from cumbersome non-decimal units to units which are simple to use and carry out calculations.

Indeed, whenever metrication had been considered in the past, it had been recognised that the full benefits of the metric system for trade would only be seen if currency also switched to a decimal system.

“Your Committee feel it to be right to add that the evidence they have received tends to convince them that a decimal system of money should, as nearly as possible, accompany a decimal system of weights and measures. Both the foreign and English witnesses think the maximum of advantage cannot be attained without a combination of the two.”

Select Committee on Weights and Measures – 15 July 1862

“Within the next ten years a large part of industry will therefore be making the change to the metric system. This reinforces the case for decimalisation of the currency. Indeed, each change increases the advantages of the other”

Decimal Currency in the United Kingdom, Government White Paper – 1966

Old money

For hundreds of years, prior to 1971, Britain used an idiosyncratic currency consisting of pounds, shillings and pence. Twelve pennies (symbol d) made one shilling (symbol s or /), and 20 shillings made one pound (symbol £).

Additionally, five shillings made one crown, and eight half-crowns made one pound. There were also coins that were fractions of a penny; the halfpenny (½ penny) and the farthing (¼ penny), and a monetary unit called the guinea, which consisted of 21 shillings. Needless to say, arithmetic in the £sd system was complicated.

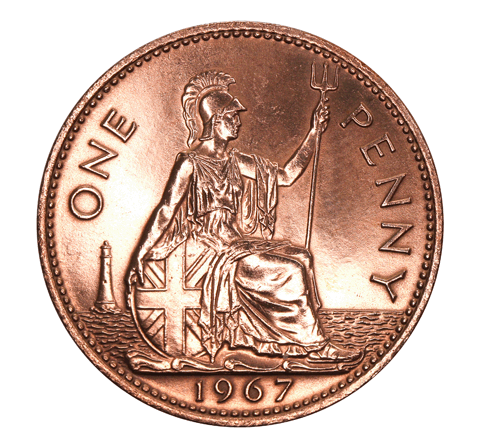

Pre-decimal money – 1967

New money

After earlier unsuccessful attempts to address the issue, a special committee was set up by the Government, in 1961, to decide whether the UK should switch to a decimal currency. The committee decided in favour of decimalisation, and on 1 March 1966, the Chancellor of the Exchequer, James Callaghan, announced that pounds, shillings and pence would be replaced by a decimal currency, with one hundred units in the pound.

Decimal money – 1971

In the new system, the pound would remain the same, but instead of consisting of 20 shillings, or 240 old pence, the pound would be made up of 100 new pence (symbol p). It followed that the one shilling coin would be equal to 5 new pence, and the two shilling coin would be equal to 10 new pence.

Transition

A single day was set for the switch to decimal currency. 15 February 1971 became known as Decimal Day, or D-Day. On this day the nation would switch from pounds, shillings and pence to pounds and new pence. However, the equivalence of certain old and new currency coins allowed for a more gradual switch over than might have been thought possible at first sight.

One shilling was exactly equal to 5 new pence, and because the size, weight and material of the 5 new pence and 10 new pence coins were identical to the their pre-decimal equivalents, it was possible for the 5p and 10p coins to be introduced while pre-decimal currency was still in use.

From 1968 onwards, one-shilling and two-shilling coins were minted with inscriptions bearing their new decimal values – 5 NEW PENCE and 10 NEW PENCE.

In preparation for the switch to decimal currency, the number of coin denominations was reduced. The old half penny (½d) ceased to be legal tender after 31 July 1969, and the half crown (2s 6d) was demonetised after 31 December 1969. Production of all pre-decimal coins ended in 1967.

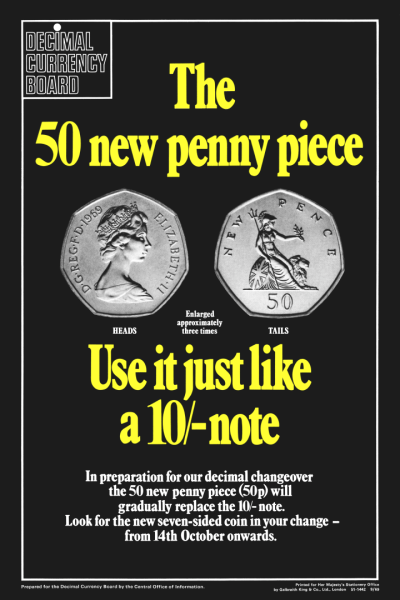

Decimalisation information poster – 1969

The 10 shilling note continued to be printed until 1969. From 14 October 1969, it was gradually replaced by a new decimal coin of equivalent value – the 50 new penny piece. The 10 shilling note ceased to be legal tender in 1970.

Coins and notes in circulation during the transition to decimal currency

| 1967 | ½d | 1d | 3d | 6d | 1/- | 2/- | 2/6 | 10/- |

| 1968 | ½d |

1d |

3d |

6d |

1/- 5p |

2/- 10p |

2/6 |

10/- |

| 1969 | ½d |

1d |

3d |

6d |

1/- 5p |

2/- 10p |

2/6 |

10/- 50p |

| 1970 | 1d |

3d |

6d |

1/- 5p |

2/- 10p |

50p | ||

| 1971 | ½p | 1p | 2p | 6d |

1/- 5p |

2/- 10p |

50p | |

| 1980 | ½p | 1p | 2p | 1/- 5p |

2/- 10p |

50p | ||

| 1982 | ½p | 1p | 2p | 1/- 5p |

2/- 10p |

20p | 50p | |

| 1985 | 1p | 2p | 1/- 5p |

2/- 10p |

20p | 50p | ||

| 1991 | 1p | 2p | 5p | 2/- 10p |

20p | 50p | ||

| 1993 | 1p | 2p | 5p | 10p | 20p | 50p |

Information campaign

A booklet was produced to inform the public about the new system. It described in detail how everyday money transactions would be affected. Copies of the booklet were delivered free of charge to every household as part of a nationwide public information campaign.

Decimalisation booklet – 1971

Decimal Day

By Decimal Day, on Monday 15 February 1971, three decimal currency coins had already been in circulation for about 2 years. This, together with an extensive public information campaign, ensured that the public would have had plenty of opportunities to familiarise themselves with the values of the new coins.

Decimal Day, or D-Day, saw the introduction of the remaining new decimal coins; the 2p, 1p and ½p, which became legal tender on that day. The two remaining “old money” coins; the penny (1d) and the thrupenny bit (3d), remained in circulation during a transition period, and were accepted for a short while in multiples of 6d (2½p). The 1d and 3d coins ceased to be legal tender after 31 August 1971.

Shopping

Logistically, it was not possible for all shops to switch to the new coinage overnight, though many did. During a transition period, prices in shops were shown in both £sd and £p. In shops that had not yet converted, it was the £sd price that had to be paid, whilst in decimal currency shops the £sd price was only a supplementary indication, and it was the £p price that had to be paid.

In the event, the majority of shops fully converted within one or two weeks, and the dual-pricing transition period lasted no more than two months, rather the 6 months that were originally envisioned.

Banks

Whilst some shops continued to operate in £sd for a short period after D-Day, all banks were required by law to complete the change to decimal currency immediately. To facilitate the change, all bank branches were closed for business on Thursday 11, and Friday 12 February. When banks re-opened on Monday 15 February, every customer’s balance had been converted to decimal currency.

Pound values remained unaltered, except for balances ending in 19s 11d which were rounded up by 1d. Every complete two-shillings converted exactly to 10p. Intermediate amounts were converted to decimal using the whole new penny Banking and Accounting conversion table.

For example £20 15s 6d became £20.77, and £56 8s 6d became £56.43.

The whole new penny Banking and Accounting conversion table

| £sd | £p | £sd | £p |

| 0d | 0p | 1/- | 5p |

| 1d | 0p | 1/1 | 5p |

| 2d | 1p | 1/2 | 6p |

| 3d | 1p | 1/3 | 6p |

| 4d | 2p | 1/4 | 7p |

| 5d | 2p | 1/5 | 7p |

| 6d | 3p | 1/6 | 7p |

| 7d | 3p | 1/7 | 8p |

| 8d | 3p | 1/8 | 8p |

| 9d | 4p | 1/9 | 9p |

| 10d | 4p | 1/10 | 9p |

| 11d | 5p | 1/11 | 10p |

As before decimalisation, banks did not deal in halfpennies.

Paying-in slips, which had three columns before decimalisation, were replaced with slips with two columns. The old three-column slips could still be used after decimalisation, with the second column being used for new pence instead of shillings, and the third column left blank.

Cheques made out before D-Day in £sd could still be paid into an account, but the value had to be converted to decimal first, with the figures for the converted value being written on the cheque above the £sd value, ideally in a different coloured ink.

Trains

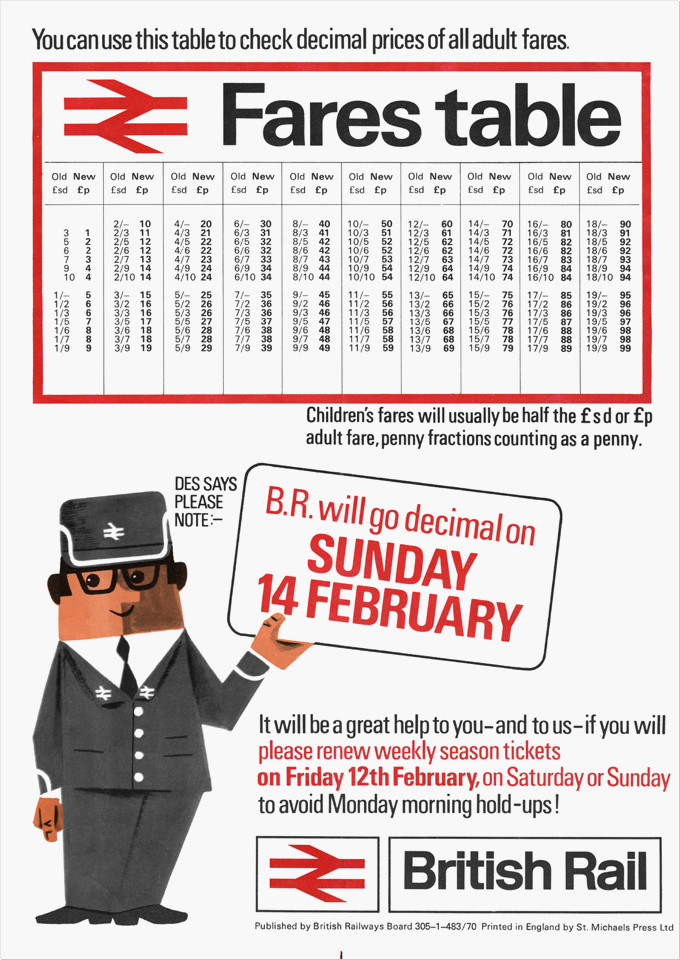

The London Underground and British Rail switched to decimal currency on 14 February 1971 – one day before D-Day.

British Rail decimalisation leaflet – 1971 |

|

Buses

Although D-Day was 15 February 1971, and the new decimal coins became legal tender on that date, bus operators were asked to remain a “£sd shop” until 21 February 1971 (D-Day + 6). This was to alleviate the possibility of a shortage of the new coins for change-giving, if they had made the switch to decimal on D-Day.

London Transport decimalisation leaflet – 1971 |

|

Some ticket machines were converted from shillings and pence to pence-only before the change over. This meant that, while buses continued to operate in £sd, fares of one shilling and over would have been shown in an unconventional format on tickets from these machines.

For example,

a fare of 1/- was shown as 12 (old) pence,

a fare of 1/1 was shown as 13 (old) pence,

a fare of 1/2 was shown as 14 (old) pence, etc.

Post Office

In 1967, the main definitive series of stamps was redesigned to incorporate an updated sculpted profile of the Queen. The same profile, by Arnold Machin, was also subsequently used on the UK’s first decimal coins.

Low value pre-decimal stamps – 1969

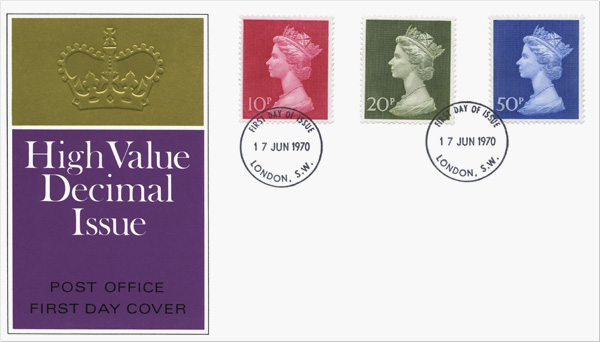

High value decimal currency definitive stamps were issued on 17 June 1970, 8 months before D-Day. This allowed stocks of pre-decimal high value stamps to be utilised as completely as possible before decimal day.

The first decimal currency postage stamps – 1970

The three decimal high value definitive stamps all had equivalent pre-decimal values that were exact multiples of shillings; 10p (2s), 20p (4s), and 50p (10s). Prior to decimal day, they were used as per their shilling equivalents.

A set of 12 low value definitive stamps was released on 15 February 1971. The launch coincided with a seven-week national strike of postal workers.

Low value definitive postage stamps – 1971

The first decimal definitive stamps featured the same Machin design as the 1967 pre-decimal definitives.

Post Office decimalisation booklet – 1971

From 15 February 1971, all Post Office charges switched to decimal currency. As with other businesses, 1d and 3d coins were still accepted during the transition period, as long as they were in multiples of 6d (2½p).

Pre-decimal stamps could be used up during the transition period following D-Day. A table gave the value of decimal stamps needed to top up various values of old stamps in order to make up the correct postage for the new first class or second class rates.

Beyond D-Day

The old sixpence (6d), with a value of 2½ new pence, was originally scheduled to be withdrawn alongside the 1d and 3d coins in August 1971, but the coin was given a last-minute reprieve and continued to be legal tender until 30 June 1980.

In 1982, the word “NEW” was dropped from the inscriptions on all newly minted coins. For example, the inscription on the 10p coin changed from “NEW PENCE” to “TEN PENCE“.

1982 also saw the introduction of the 20p coin.

By the early 1980s, following a period of high inflation, the ½ new penny coin had become so devalued that it was decided to withdraw it from circulation. It was demonetised in December 1984. The UK finally had a purely decimal currency.

After D-Day, the old one-shilling and two-shilling coins had continued to circulate alongside their equivalent coins, the 5p and 10p. In 1990 and 1992 respectively, the sizes of the 5p and 10p coins were reduced. The older and larger versions of the 5p and 10p coins, together with the old 1s and 2s coins, were subsequently removed from circulation.

It seems fitting that the florin, which had been introduced in 1849 as the first nominally decimal coin, with its original inscription “ONE TENTH OF A POUND“, rather than “TWO SHILLINGS“, was also the last pre-decimal coin to be demonetised. It ceased to be legal tender when the older and larger version of the 10p coin was withdrawn from circulation on 30 June 1993.

Numerical symbols

One of the novel features of the coins introduced for decimalisation, that is often overlooked, was that their values were indicated using standard numerical symbols. Hitherto, coin values were shown in words alone.

Before decimalisation, anyone encountering British coins for the first time not only had to know how crowns, shillings and pence related to pounds, but also had to ask what a coin’s value was if they could not understand its English language inscription.

The introduction of coins with values shown clearly using conventional numbers was a massive boost for child numeracy. School children learning about money, and how to add up, could easily relate to the numbers on the coins.

However, in 2008, a redesign of definitive coins saw a regression to values being shown in English language text only. Numeral values were removed in favour of an amusing design that enabled a complete set of the different coins to be arranged like a jigsaw to form a picture of a shield.

Decimal coins – 2022

It was another fifteen years until this retrograde step was reversed. Universally-understood numerical symbols were finally re-introduced when new definitive coins were designed for the new monarch.

Decimal coins – 2023

In 2023, when the new coins were announced, the director at the Royal Mint said, “The large numbers will be very appealing to children who are learning to count and about the use of money“.

The benefits of decimalisation

The benefits of decimalisation were described in the Government white paper on decimalisation presented in 1966:

5. Decimalising the currency will be an important aid to productivity. In ordinary arithmetic we count in tens; in £ s. d. money calculations we count in twelves, twenties and tens. Decimalisation of the currency will bring about a harmonisation of money and non-money calculations and, as a result, money calculations will be quicker, easier, and less prone to error. Savings will occur in all walks of life. All will benefit. For shoppers and shop assistants the mechanics of payment and change-giving will be streamlined. But the most obvious savings will occur in offices and in schools.

Office work and office machines

6. In offices – and of course in banks – the mental and paper work of monetary calculation will be greatly simplified. In addition, all the aids available for ordinary calculation, ranging from slide rules and log tables to adding and accounting machines, will also be usable for money calculation. Special £ s. d. monetary machines will no longer be needed and this advantage will be increased by the fact that a decimal notation is more economical than our £ s. d. system in its use of figures, making it possible to use cheaper machines of lower recording capacity. Because almost all other countries have decimal currencies, £ s. d. monetary machines are non-standard; manufacturers have to produce special models for the United Kingdom market. When we have a decimal currency most machines will be standard; this should enable our manufacturers to keep down costs and to compete more easily abroad. A wider choice of machines, of both home and foreign manufacture, should be available to the machine user.

Schools

7. The educational benefits of decimalisation have always been regarded as an important reason for making the change. Much time in primary schools is devoted to teaching children the special rules of money arithmetic. When a child has learned the basic decimal processes of addition, subtraction, multiplication and division, he has to learn different methods for dealing with money sums; the process is tedious, time-consuming and lacking in intellectual excitement. When we have a decimal currency, teaching time will be saved and text books will be simplified. Some of the early disenchantment with mathematics often experienced by school children may be avoided, and the change will fit in well with changes already taking place in mathematics teaching. Educationalists, in their evidence to the Halsbury Committee, stressed, however, that the full benefits of a decimal currency would only be obtained in conjunction with a full metric system of weights and measures.

The metric system

8. In May 1965 the President of the Board of Trade announced that the Government considered it desirable that British industries, on a broadening front, should adopt metric units, sector by sector, until that system could become in time the primary system of weights and measures for the country as a whole. Within the next ten years a large part of industry will therefore be making the change to the metric system. This reinforces the case for decimalisation of the currency. Indeed, each change increases the advantages of the other and, taken together, they should help exports because most of our overseas markets already use the metric system and have decimal currencies.

Measuring the savings

9. The benefits described in paragraphs 5 to 8 will undoubtedly lead to substantial savings of time and effort in offices, banks, shops and schools. Although these savings are important, there is no easy way of expressing them in money terms. So far as office work is concerned, the Institute of Office Management told the Halsbury Committee that they believed it likely that the cost of the change-over in offices would be recouped in savings within a year or so from the date of the change. For schools, the saving in mathematics teaching time for the 6 to 11 age group has been estimated at roughly 5 per cent to 10 per cent or 2 per cent of total teaching time. But decimalisation will not reduce the number of clerks, still less the number of teachers; it will simply mean that those we have are employed more effectively. Many of the benefits of decimalisation will make themselves felt in the same way as productivity or technical changes-diffused over the economy, not always easy to identify, but none the less of great practical significance. Experience in South Africa has confirmed that the benefits expected of decimalisation can be achieved in practice. The Report for 1965/66 of the Australian Decimal Currency Board points out that, after less than five months experience, many organisations already claim to be enjoying the benefits.

Earlier attempts at decimalisation

The first step to a decimal currency was taken in 1849, with the introduction of the florin, which had a value of 1⁄10 pound, or two shillings.

The 1849 Florin – ONE TENTH OF A POUND

At that time, it was proposed that the farthing (1⁄960 pound) should be replaced with a new decimal coin of similar value, the mil (1⁄1000 pound). The halfpenny and penny would have been replaced by new “copper” coins of 2 mils and 5 mils. Most existing silver coins would have had exact equivalent values. Thus 6d = 25 mils, 1s = 50 mils, 2s = 100 mils.

19th Century proposal for decimal currency using £ and mils (1 mil = £0.001)

| Coin | £sd | £ | Farthings | Mils |

| Crown | 5s | 1⁄4 | 240 | 250 |

| Half crown | 2s 6d | 1⁄8 | 120 | – |

| Florin | 2s | 1⁄10 | 96 | 100 |

| Shilling | 1s | 1⁄20 | 48 | 50 |

| Sixpence | 6d | 1⁄40 | 24 | 25 |

| Threepence | 3d | 1⁄80 | 12 | – |

| Penny | 1d | 1⁄240 | 4 | – |

| Halfpenny | ½d | 1⁄480 | 2 | – |

| Farthing | ¼d | 1⁄960 | 1 | – |

| 10 mils | – | 10⁄1000 | – | 10 |

| 5 mils | – | 5⁄1000 | – | 5 |

| 2 mils | – | 2⁄1000 | – | 2 |

| 1 mil | – | 1⁄1000 | – | 1 |

Further attempts to kick start decimalisation included the introduction of the double florin (2⁄10 pound) in 1887. However, political will again failed to see through the change, and the country had to wait more than 100 years for the final switch to a decimal currency.

Alternative decimal currency systems

The 1961 Report of the Halsbury Committee weighed the merits of 25 systems, four of them in detail. However, the Committee soon decided that the final choice should be between the “£-cent-½” and the “10-shillings-cent” systems.

Much of the case for a “10s-cent” system stood on what the Halsbury Committee called “associability”. This referred to the ease with which it would have been possible to translate sums of money from £sd to decimal, and back, during the transition.

Under the “10s-cent” system, shilling and penny “shopping prices” could be translated easily, coinage changes would be fewer, and no fraction of the minor unit would have been needed. The “associability” factor of having an exact equivalence of shillings and tens of cents favoured the “10s-cent” system. However, none of the old units would have been retained.

The “£-cent-½” system, on the other hand, had the advantage of retaining the familiar major unit.

When other Commonwealth countries converted their currencies, some took the “10s-cent” route. In the case of Australia and New Zealand, the internationally familiar “dollar” and “cent” were adopted as unit names.

In 1966, the British government decided on the “£-cent-½” system, opting to retain “penny” as the name for the new cent coin. Maintaining the long term continuity of the major currency unit was considered to be more important than any short term advantages that the “10s-cent” might have had during the transition period.

The following table summarises some of the pros and cons of each system. Many of the issues were of relevance only during the transition process.

| “£-cent-½” system | “10s-cent” system |

| The pound is retained. No changes to existing bank notes. |

All three £sd units are replaced. All banknotes replaced by new banknotes in “dollars”. No obvious candidate for the name of the new major unit (suggestions included “dollar”, “royal”, “britannia”). |

| 6d coin becomes an awkward value (2½ new pence). |

6d coin can be retained as 5 cents. |

| New coins needed to replace ½d, 1d, 3d and 6d coins. |

New coins needed to replace ½d, 1d and 3d coins. |

| ½ new penny needed. This involves additional work when written or printed, whether it is expressed as ½, or as a third decimal place. It also means an additional non-standard column on some business machines. However, it was correctly anticipated that the ½ new penny would eventually be dropped. |

No ½ cent needed. |

| Less “associability” for small amounts: 1 new penny has a value of 2.4 old pence, 1 shilling becomes 5 new pence. |

Greater “associability” for small amounts: 1 cent has a similar value to 1 old penny, 1 shilling becomes 10 cents. |

| “Shopping prices” are less readily translated: e.g. 1s becomes 5 new pence. 1s 6d becomes 7½ new pence. 2s becomes 10 new pence. |

“Shopping prices” are more readily translated: e.g. 1s becomes 10 cents. 1s 6d becomes 15 cents. 2s becomes 20 cents. |

Comparison with metrication

Decimalisation in the UK has taken a similar path to that of metrication. However, each process has met with different degrees of success.

| Decimalisation | Metrication |

| First steps taken in 1849, with the introduction of the £0.10 florin coin. | In 1895, the Report from the Select Committee on Weights and Measures recommends that the metric system be legalised for all purposes, and be rendered compulsory by 1897. |

| In 1966, the Government announces its intention to switch to decimal currency in the UK. | In 1965, the Government announces its intention that within 10 years the greater part of the country’s industry should have changed to the metric system. |

| In 1967, the Decimal Currency Board was established to oversee the change. | In 1969, the Metrication Board was established to oversee the change. |

| Extensive planning and an intensive short publicity campaign precede a quick changeover period, backed up with decisive legislation. | A gradual, and mostly voluntary, approach is taken. Sparse publicity. Most successful when consensus has been backed up with legislation. |

| Generally agreed to be a great success. | The process is drawn out over many decades. The absence of visible government support allows resistance to grow. Some sectors complete the change successfully, but the full benefits of a nationwide adoption of a single measurement system are yet to be achieved. |

| The UK was the last major country in the world to switch to a decimal currency. | If the USA acts before us, the UK will be the last major country in the world to switch road signs to metric units. |

FUN FACT :

In old money, there were 63 groats in 1 guinea.